Prelude

The world is entering a phase of slower growth. The World Bank projected that global growth will only reach 2.7% this year, warning that such a low growth rate would not encourage continuous economic development.

Although inflation rates have stabilised and most countries are now applying monetary-easing policies, the uncertainty surrounding the trade war between the United States and the rest of the world, as well as ongoing conflicts and genocide in various regions, will impact the growth and the outlook trajectory of ASEAN countries in the near to medium term.

Is the United States Still a Trade Partner?

The United States remains an important market for ASEAN, being ASEAN’s second biggest trade partner in terms of exports (outside of ASEAN), just behind China. In 2023, exports to the United States reached US$309bn, while exports to China and Japan reached US$350bn and US$120bn, respectively.

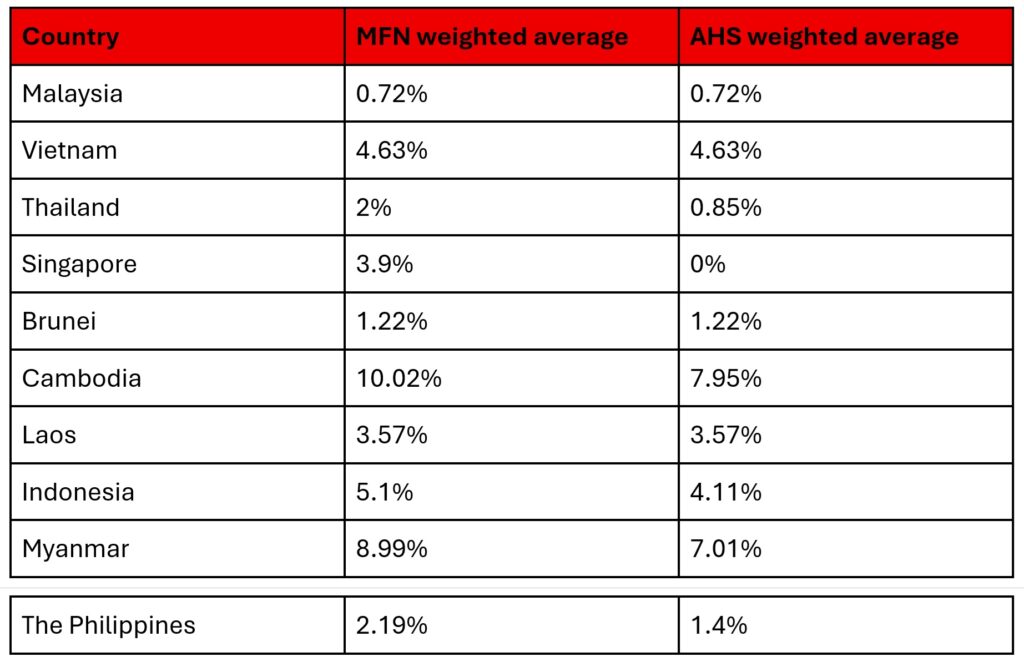

The boom of ASEAN’s trade with the United States was marked by lower levels of tariffs in 2022 in terms of both Most Favoured Nation (MFN) and effectively applied weighted averages.

In that year, the MFN weighted average was even lower than the proposed blanket tariff of 10% that was later proposed. For most ASEAN countries, the MFN weighted average tariff did not exceed 10%, except for Cambodia.

Nevertheless, when we look at the effectively applied weighted average tariff, the rate went below the MFN weighted average for six out of the 10 ASEAN countries, namely Thailand, Singapore, Cambodia, Indonesia, Myanmar and the Philippines.

In short, the applied tariff rates were either the same or much lower than the agreed MFN tariffs when weighted against the actual value of ASEAN products imported into the United States.

Table 1: Most Favoured Nation (MFN) and effectively applied weighted averages for ASEAN countries in 2022

The United States imports electrical machinery and equipment, industrial machinery and components, and furniture and bedding, among others, from ASEAN. For electrical, machinery and equipment alone, the United States sources these products from Vietnam, Malaysia, Thailand, the Philippines, Indonesia, and Laos. Not surprisingly, Vietnam, Malaysia and Thailand were the biggest exporters of these products to the United States, amounting to US$94.06bn.

Despite the long-term trade ties and ASEAN’s competitive advantage in producing exportables attractive to American consumers, the recent announcement of high tariffs in April 2025 are seen as an aggressive and unjustified move to rectify trade balances. Such is an unfair trade practice, which is ironic indeed.

High Tariffs and Their Impacts

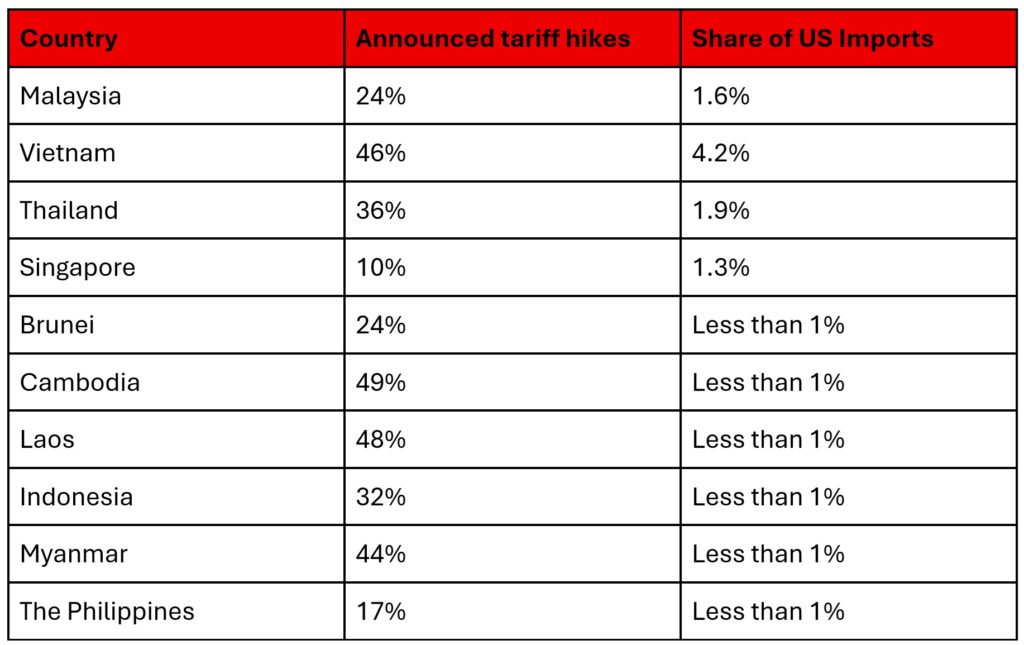

Table 2: The tariff hikes announced in April 2025 to remedy trade imbalance, initially to be implemented on the 9 April 2025, but later pushed to 8 July 2025.

The highest tariffs announced were targeted towards Vietnam’s, Cambodia’s and Laos’ exports to the United States at 46%, 49% and 48%, respectively. The high tariffs, however, were not justified by the share of US imports. In the table above, countries like Brunei, Cambodia and Laos, whose exports account for less than 1% of US imports, were slapped with tariffs ranging from 24% to 49%.

Countries are rushing to negotiate because there are negative implications of higher tariffs in the short to long term.

In the short term, the unilateral tariff hikes will force producers and exporters to operate on a narrower profit margin. This happens through the difference between the world price and the domestic price of a given good, like the semiconductor, especially when tariffs are introduced by a big economy, like the United States.

The higher tariffs on semiconductors will impact American consumers’ demand domestically, which will further dampen the world’s demand for the product. These changes will then result in lower world prices for that product.

As producers and exporters in ASEAN need to grapple with lower world prices of semiconductors, they will also need to compete with each other or other producers on the basis of cost per output. With subdued global demand, it is difficult for producers and exporters to scale up or expand their production in the medium term. The situation, then, becomes a catch-22 conundrum. Both output and productivity will be impacted negatively.

In the short to medium term, drastic tariff hikes may lead to an increase in inflation in the United States. This could delay the rate cuts by the Fed, whose moves act as guides to local monetary policies in most ASEAN countries. Such delays may impact ASEAN’s exporters and the availability of affordable financing locally. Besides that, when inflation is expected to increase, frontloading of spending is also observed in the short term, as observed in recent months.

In the long term, tariff hikes have a more detrimental outcome not just for the United States but also for ASEAN exporters. A study has found that this protectionist move can lead to higher unemployment and higher inequality in the United States. It also found that tariff hikes have a small impact on rectifying trade balance and are therefore rendered ineffective.

Furthermore, as exporting countries, ASEAN member states may experience higher unemployment rates in the affected sectors if producers continue to depend on the United States as their sole market destination and are forced to compete with other neighbouring countries aggressively, without trade diversification strategies in place.

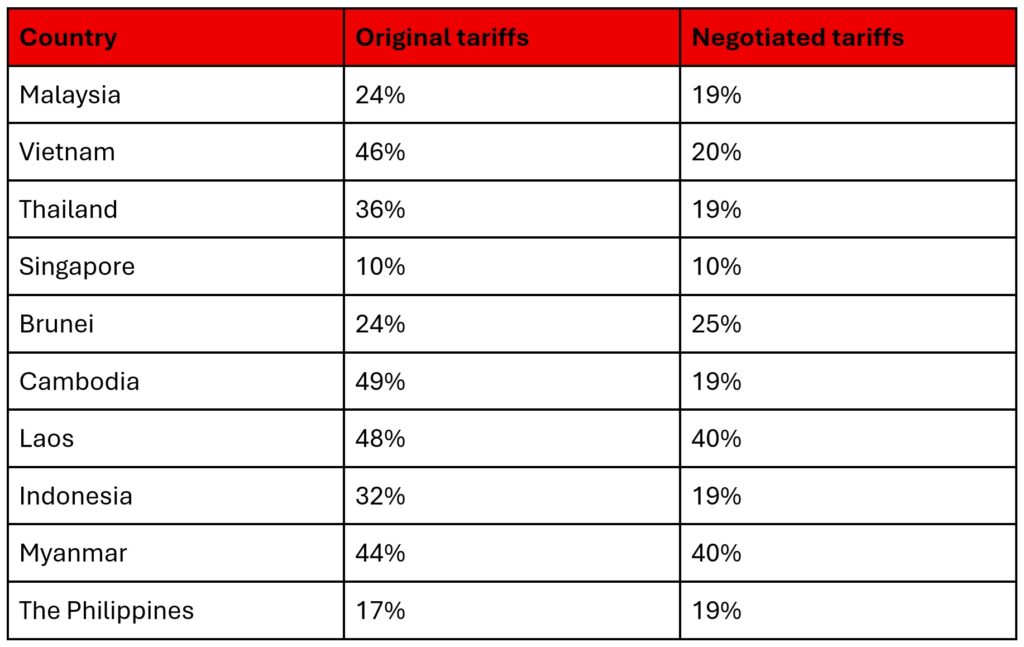

Despite the announced tariff hikes, ASEAN member states have recently managed to secure lower tariffs from the United States, though this is not the case to all.

Table 3: The recently announced tariffs for ASEAN countries after months of negotiations.

High Costs?

As the United States aims to correct its trade imbalances with ASEAN countries, other terms, including non-tariff barriers and investment commitments, were also included.

What was the cost paid by selected ASEAN countries in securing these lower tariffs, and most importantly, did these countries give in too much for the sake of relatively lower tariffs for their exportables to the United States?

For Malaysia, the cost of securing a lower tariff of 19% was different investment and purchase commitments, including 30 Boeing planes, coal and telecommunication equipment valued at more than US$240bn. While telecommunication equipment imports may support Malaysia’s digitisation and automation journey, coal imports may hamper Malaysia’s net zero-carbon journey by 2030.

Additionally, with Boeing’s below-par safety track record, these purchases may not be the best decision made in strengthening Malaysia Airlines’ (MAS) somewhat weak reputation, even if the airline was making a profit three years in a row. As part of the trade deal, Malaysia needs to comply and purchase the planes, giving little room for manoeuvring even if new risks were to be discovered related to Boeing’s performance.

Malaysia has also eliminated tariffs on approximately 98% of all goods imported from the United States. Moreover, the easing of selected non-tariff barriers (NTBs), specifically on the halal certification process, and the exemption for US social media platforms and cloud service providers to contribute 6% of their weighted net revenue to the Universal Service Provision (USP) fund in Malaysia, were also agreed upon.

While the halal certification process needs to be improved in terms of transparency and capacity in general, the exemption of contributions from US tech firms is a huge blow for Malaysia, as the revenue from this sector is projected to be significant. This exemption will be applied to digital products and digital services provided by companies such as Apple, Google Play, Netflix, and Microsoft, among others.

Apart from Malaysia, Indonesia has also committed to the purchases of Boeing planes as part of the trade deal, apart from purchasing energy and agriculture products from the United States. On NTBs, Indonesia also agreed to reduce cumbersome licensing requirements. And on tariffs, Indonesia has also agreed to eliminate tariffs on 99% of imported goods to secure a 19% tariff with the United States.

At the time of writing, Trump had just announced that imported semiconductors will face up to 300% tariffs. This brings us back to the question of whether we gave in too much, given the fact that Malaysia’s semiconductor exports to the United States were valued at RM60.6bn in 2024.

This figure represents about 50% of Malaysia’s total electrical and electronic (E&E) exports to the United States and about 20% of Malaysia’s total semiconductor exports. The same question applies to Indonesia, especially when total trade with the United States in 2023 only represented around 8% of the total Indonesian exports.

Uncertain Future

As the agreement is still being finalised at the time of writing, and no detailed information has been published on the concessions made, to prepare for the uncertain future and possible tariff hikes by the United States in the medium to long term, ASEAN exporting countries need to explore avenues that can minimise their risks.

As the trade war will impact the supply chain immediately, a reconfig

Presently, ASEAN countries are party to many FTAs, yet not all of them are being utilised optimally. Moreover, exploring new partner countries for cooperation and trade can reduce reliance on the highly uncertain and volatile US market. Recently, ASEAN has signalled its interest in signing on to the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) to widen its network of trade partners in this region and beyond.

In the medium to long term, ASEAN exporters and producers need to build on their competitiveness and comparative advantage. If an exporter is no longer able to compete based on cost per output, a product diversification strategy is needed to differentiate its product from other substitutes.

In the long term, apart from product diversification, ASEAN exporters and producers need to move up the value chain to produce products with higher value-added content. This is another way to differentiate their products from other substitutes.

While ASEAN has separately negotiated with the Trump administration to safeguard ASEAN’s centrality and to protect its regional supply chain, a collective negotiation approach by all ASEAN member states in the future needs to take place. Instead of focusing on securing the lowest tariffs with the United States, ASEAN needs to work together as a unified economic region, as outlined by its many blueprints. While the next decade may be a daunting future full of uncertainties, preparation is key. Shifting to a newer way of doing business may drive costs up in the near future, but with time and know-how, these costs will decrease over time, and the benefits of reducing dependency on the United States will be felt by affected sectors and their players.